Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

I have seen the future!

Series – The Online Gambling Industry

Programmers unlock the future

I was recently asked to technically review a new online sportsbook system by a group of talented and enthusiastic programmers. This kind of task is right up my alley as you can imagine and one I thought would not take me too much time out of my relatively short, but (so far) warm summer. However, what I have been presented with so far has blown my little technical socks off and I’m hooked.

This new sportsbook’s proponents are a young team – most of whom are a third of my age – but that does not seem to have negatively affected the technical know-how needed to create a new sportsbook. Indeed I would argue that their youthfulness has given them the ability to provide a totally fresh look on the whole subject. And it has worked in their favour.

My summary of their work at this stage would be – I have seen the future, yet again!

But before I go into some detail of just what I have seen, let’s just go through where we are right now.

The story of sports betting is almost as old as sport itself. Long before modern sportsbooks, mobile apps and live betting, people were already wagering on contests of strength, speed and skill.

Evidence of gambling dates back thousands of years. Archaeologists have discovered dice and gaming artifacts from ancient Mesopotamia dating to around 3000 BCE. As organised sporting contests emerged, betting naturally followed.

In Ancient Greece, spectators at the Olympic Games and other athletic festivals frequently wagered on the outcomes of races, wrestling matches and chariot events. These bets were often informal, but they demonstrated a human instinct that has remained remarkably consistent throughout history: the desire to predict a result and stake something on being right.

The Romans elevated sports betting to a new level. Throughout the empire, wagers were placed on gladiatorial contests, horse races and, most notably, chariot racing. The Circus Maximus in Rome, capable of holding hundreds of thousands of spectators, became one of the earliest centres of organised sports betting. Racing factions such as the Blues, Greens, Reds and Whites attracted passionate supporters who bet heavily on their favourites.

Betting became so widespread that Roman authorities periodically attempted to regulate or restrict gambling. Despite these efforts, wagering remained deeply embedded in Roman society.

Following the fall of Rome, betting survived throughout Europe, although often in conflict with religious authorities. Medieval rulers and church leaders frequently condemned gambling, viewing it as a moral vice. Nevertheless, people continued to wager on tournaments, jousting competitions, archery contests and other popular events.

Like many forms of gambling throughout history, sports betting often moved underground when prohibited, only to re-emerge when attitudes softened.

Modern sports betting owes much to horse racing. During the 17th and 18th centuries, horse racing became increasingly popular among the British aristocracy. As racing grew, professional individuals began accepting and recording bets. These early operators became known as “bookmakers” because they kept betting records in books.

By the late 18th and 19th centuries, betting markets had become more sophisticated. Odds were calculated, betting houses appeared, and organised wagering became a recognised industry. The expansion of newspapers, telegraphs and later telephones allowed bookmakers to distribute information more quickly and operate on a larger scale.

Harold Macmillan legalised bookmaking in the UK

The twentieth century saw sports betting move steadily into the mainstream. Governments increasingly recognized that prohibition was ineffective and that regulation could provide both consumer protection and tax revenue.

In the United Kingdom, betting shops became a familiar part of everyday life. Football pools, horse racing wagers and fixed-odds betting transformed gambling into a mass-market activity. Similar developments occurred in various forms across Europe, Australia and other regions.

Television further accelerated growth. Sports became global entertainment products, attracting larger audiences and creating new opportunities for bookmakers.

Intertops.com started the Internet betting bonaza

The most significant transformation arrived in the 1990s with the commercial growth of the Internet. For the first time, bettors could place wagers without visiting a betting shop or casino. Online sportsbooks emerged, offering unprecedented convenience, wider betting markets and access to international customers.

Among the pioneers was Intertops, widely recognised as the world’s first online sportsbook. During its formative years, I was directly involved in the development and operation of the business, witnessing first-hand the challenges of bringing traditional sports betting into the digital age. At the time, many of the technologies, payment systems and regulatory frameworks that are taken for granted today simply did not exist. The industry’s early pioneers were effectively building an entirely new sector from scratch.

What began as a small number of experimental websites quickly evolved into a global industry serving millions of customers across multiple jurisdictions.

The next major technological shift emerged with blockchain technology and cryptocurrencies. While online sportsbooks had already transformed the distribution of betting services, blockchain introduced the possibility of transparent betting ledgers, digital assets and decentralised payment systems.

In the late 2010s, I became involved in the creation of Betr.org, one of the first sportsbooks built around blockchain technology. The project sought to explore how distributed ledger systems could improve transparency, efficiency and trust within sports betting.

Blockchain betting remains the most exciting and rapidly evolving sector of the sports betting industry and is indeed the subject of this article.

The future was P2Predictable

I have predicted the future of sports betting a couple of times before. I was definitely at least right one time with my dogged insistence in 1994 that Internet betting was the way forward.

Luckily I was in a position to prove myself right as I had the technical ability to go out on a limb and write the software that ran the first online sportsbook Intertops.com.

The second time I thought I knew the future was in the late 2000’s when I started becoming fascinated by Peer-to-Peer (P2P) betting, that is direct betting between bettors with no middleman i.e. cut out the bookmaker. The idea was not mine I have to admit – Betfair’s Exchange had been operating since 2000 and that allowed bettors to offer and place bets with each other. However, they still needed a centrally run system to operate.

But the idea that bettors themselves could create their own offers in a sort of democratic marketplace still appealed to my technical and independent self. So, I asked myself the question, could it be possible to eliminate the middleman entirely and enable bettors to bet directly with each other?

I dabbled in the subject by creating a few smartphone apps that supported the idea of P2P betting to see if there were some legs to this subject. I had some fun with this and learned a lot. Unfortunately, one big thing I learned was that although functional, P2P betting markets were not easily fundable as it is unclear as to who and how one’s bread is buttered – cutting out the middleman effectively cuts out the revenue. And as a result, no one else was interested.

Adriaan Brink

So back to the drawing board? Not exactly. Enter the legendary Adriaan Brink! I have written about Adriaan in a number of my previous articles. He was a true visionary and a friend to many in this industry. So sadly missed.

Adriaan also saw the P2P light and after many conversations (with many beers) we came to the idea that P2P betting should be possible by enabling one person’s smartphone to talk directly to another person’s smartphone without using any kind of service between them.

This was the nature of the Internet right? One IP address can send data packets to any other IP address so allowing a conversation between two devices. So sending betting data between two smartphones should be possible.

Of course it’s not that simple. Theoretically it’s possible, but practically it’s not because there’s these pesky things called firewalls that sit in the way of data traffic, happily defending their designated devices from uninvited data packets.

But surely there must be a way. Services such as Skype (in those days) made it possible for a PC to talk to another PC using the Internet. Were the PCs not directly connected to each other? The answer is – sometimes.

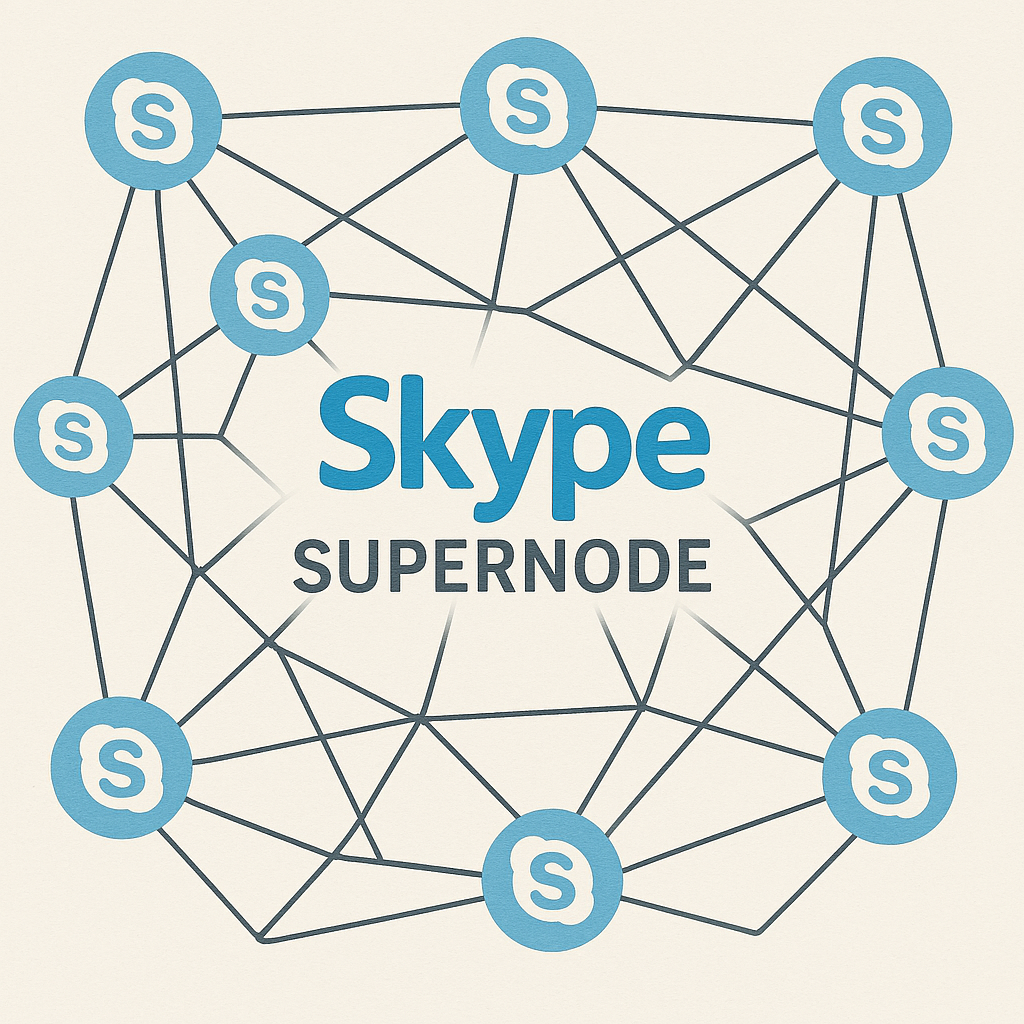

Skype software enabled employed supernodes that enabled PCs to connect directly

The early version of Skype used a network of “supernodes” which acted as a directory service (any computer that had installed Skype could become a supernode depending on it’s accessibility and capability). When one logged in to Skype your IP Address was sent to a supernode along with the open ports that your computer could be contacted on.

Making a Skype call to your mate would involve the software looking up your mate’s directory entry lodged on a supernode to ascertain their IP Address and an available port to establish a direct connection. All good if it worked. If it didn’t then the call data packets would be routed through the supernode which was made possible because when you logged in and you connected to the supernode, the connection was maintained – it could subsequently be used to send voice data and so the user could send and receive calls via the supernode.

This all worked just fine and Skype became the #1 Internet telephony app. Anyone could call anyone for free which made a lot of traditional phone companies very worried indeed.

However, when Microsoft acquired Skype in 2011 for $8.5 billion, the peer-to-peer design became a problem. Issues included difficulties with regulatory compliance as it was hard for law-enforcement to intercept calls. And technically it had performance problems as there was an increasing demand for video calls which often strained the call-routing supernodes (for which a smartphone was poorly suited).

So, Microsoft gradually migrated Skype to a cloud-based architecture and it ended up being a minnow in a pond of bigger Google and Facebook fish. Microsoft decided to pulled to pull the plug and that was the end of Skype.

But could the communications techniques that Skype used also be used for a P2P betting network?

Skype’s supernode model solved three things: discovery, connectivity and routing. For betting purposes, the model could be adapted to distribute market information, broadcast communications and match counter-parties. So far so good!

But there is a big difference between communicating a voice call and a bet. Voice calls are continuous streams of data, and you don’t care If you occasionally miss a bit or two – the call will still be understandable.

On the other hand a bet is a financial transaction and you do care very much about data integrity. Not only that, the Skype model lacked an intrinsic authentication mechanism and therefore cannot be trusted with transactions that involve currency.

So Skype did not solve the key issues of trust and settlement. But then we learned of the Blockchain which could cleverly solve all these issues.

Ethereum Blockchain introduced Smart Contracts

By this time around 2016, blockchain was in it’s infancy. Bitcoin was hot and it had proved that one could send some non-physical thing of apparent value to another without the use of an intermediary such as a bank. It did this by employing some very clever cryptographic techniques and a decentralized network of miners which kept a public ledger (the blockchain) up-to-date.

However, Bitcoin is not exactly what we needed to create a P2P betting network. For sure Bitcoin solves authentication and the payments sides of the issue (albeit very slowly) but what we also needed was something like a database to store bets and that it could be programmable.

Our desires were met by the introduction of the Ethereum Blockchain. Ethereum was proposed in late 2013 by Vitalik Buterin, who believed blockchain technology could be used for much more than payments.

The Ethereum network launched in 2015 with a revolutionary concept: smart contracts. Instead of simply recording ownership of money, Ethereum could execute programmable agreements directly on the blockchain. Developers could build decentralized applications (dApps), issue digital assets, and create entirely new financial systems without relying on traditional intermediaries.

Being Public Means It’s Complicated

Just what we needed it seemed – a publicly available system which could be trusted, could handle value, could be programmed and, most importantly was decentralized and therefore unstoppable.

A financial transactional data-based system – such as sports betting is – is an ideal application for Ethereum.

But. Ethereum is very tricky to program and, as an old programmer that I am, you had to adapt to this new secure environment where permissions were everything. And one small error in your Smart Contract meant you could lose it all.

Nevertheless, despite the learning curve, we set about the task of creating a P2P sportsbook and employing Ethereum Smart Contracts as much as we could.

We defined a system that would enable anyone to be able to offer bets and for anyone to place bets. And for payments, we wanted to use our own currency which was also a way to raise some needed financing.

Luckily for us, the introduction of Ethereum also enabled anyone to create their own currency tokens or coins which could be minted by us, exchanged for hard cash during a process called an Initial Coin Offering (ICO) which was a bit like an IPO. Issued tokens could then be traded on specialised crypto currency exchanges and would hopefully rise in value.

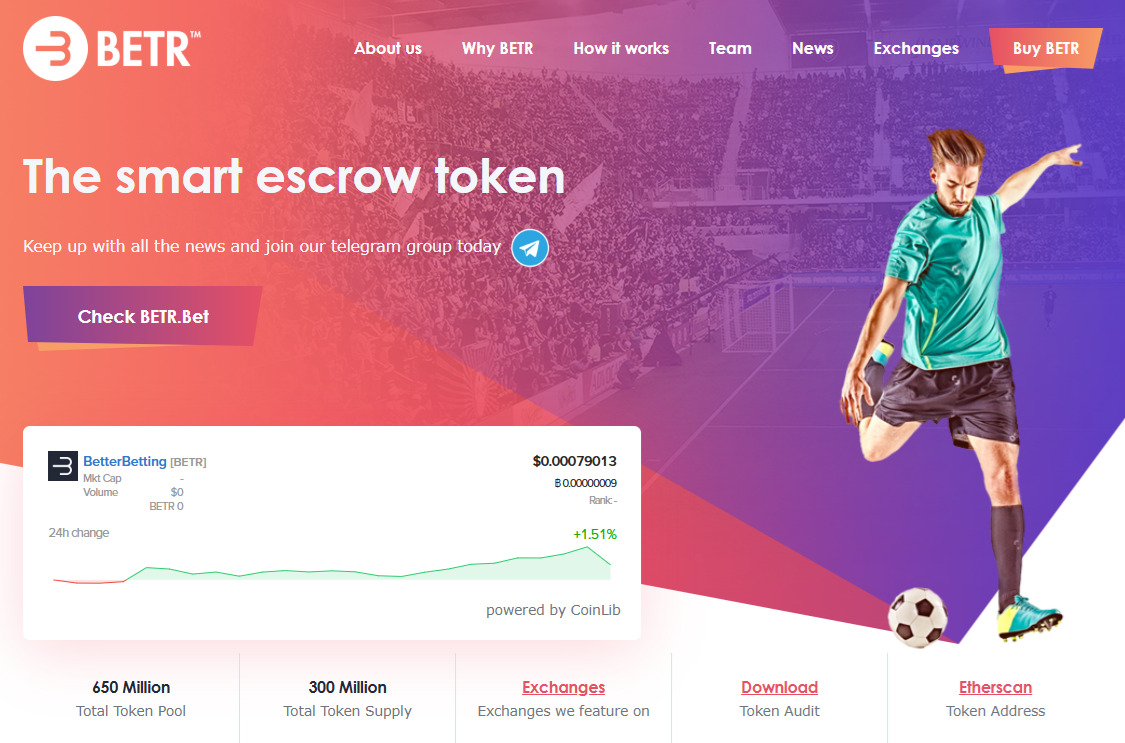

BETR.org created the first true blockchain sportsbook but had a deadly flaw

Creating a P2P sportsbook on Ethereum was not easy by any means. BETR.org was among the first generation of blockchain sportsbooks and one of the earliest projects to apply smart contract technology to P2P sports betting. And we soon learned of Ethereum’s severe limitations that had an impact on the design of the system.

Firstly, Ethereum was lousy at storing large quantities of data. Not only was it expensive but it nigh on impossible to do so. This meant that anything other than the barest of information was not going to be possible to reside on the blockchain – so, only the actual bet data would be store-able.

This meant that we still needed a traditional database to store the huge amount of event data at the very least.

Secondly, there is the issue of gas. A constant worry believe me I know, but in terms of Ethereum the issue was more profound. The creator of a transaction – such as placing a bet – would need to pay for the transaction using the native currency of the Ethereum blockchain which, unsurprisingly, is called Ethereum (ETH).

It cost a lot to place a bet

Each transaction on Ethereum (apart from transferring ETH) generally involves calling a function that is defined in a smart contract (such as placeBet()) and the cost thereof is related to the complexity of the function being called. In other words, the more work the blockchain does, the higher the cost. The term gas is used by Ethereum to directly relate the complexity of the transaction to the cost in ETH.

For example, a simple coin transfer from one persons wallet to another would cost, maybe, 21,000 gas which in the early days when ETH cost virtually nothing would be around 5 cents – if that.

So, regardless of the type of transaction, you need a balance of ETH to pay for the transaction. Therefore, there is a need for a bettor that wants to place a bet to not only have some BETR tokens to bet with but also to have a balance of ETH to pay the gas fee for the transactions.

This was a real hurdle and one we solved (seemingly) by creating a website for bettors (with the usual create account, login & password) where they could see all the bet offers and place their bets. The website would also act as their wallet where they could store their BETR tokens and where we could send some ETH to pay for the transactions.

In this way, the Bettor only needed to worry about having enough BETR tokens to pay for their bets and didn’t need to have to top up their ETH to pay for the Ethereum transactions.

Blockchain wallets store your keys not your crypto

Now I have mentioned the term wallet a few times, I need it to explain to the uninitiated. To be absolutely clear though, a blockchain wallet does not store any value such as crypto tokens – those are actually just balances held on a smart contract. A wallet only stores your blockchain keys.

Perhaps the term wallet is a misleading in this regard and the term Key Holder might be better suited. However, ‘tis wot it is.

The standard definition of a blockchain wallet is as follows:

A software or hardware application that manages cryptographic key pairs and enables users to sign blockchain transactions, thereby controlling assets and interacting with decentralized networks.

To explain: When you want to interact with the blockchain, you need an identity to prove you are who you say you are. As you can imagine, a public computer – which the blockchain is – needs unbreakable security as everything is open and available to everyone. Potentially a hackers paradise.

The blockchain is a bit like the world around us in that there are many places you can go – in theory anywhere on earth – but you will need some sort of key to open closed doors an thus gain access.

It’s the same in Blockchain, you need a key! Except that rather than being made of a bit of metal, a blockchain key is a long and totally unmemorable string of characters and numbers. So, to take care of your key you need an application called a wallet.

Now it gets a bit clever. The key that you store is known as the Private Key as only you have access to it and no one else ever sees it. And yes, you guessed it, there is also a Public Key (which is mathematically derived from the Private Key using a one-way cryptographic function).

Everyone can see your Public Key and it can be used to identify you (for example as an account id) as your public key can be verified by deriving it from some data that was signed by your private key.

Sign with your key

Oh yes, signing. In order to verify you, you sign stuff using your Private Key as I said. For example, you want to place a bet and that (in the BETR case) involves you calling a placeBet() function on a smart contract and sending some BETR tokens along to pay for the bet.

This ‘stuff’ is called a transaction and, as it does something important, it needs to be signed using your Private Key – the signing process takes the transaction data along with your private key and creates a digital signature which is another long string of character and numbers. The digital signature is sent to the blockchain along with your transaction.

On arrival at the blockchain, the transaction and signature are checked to see if they are mathematically correct and that the sender corresponds to the derived Public Key. It also checks that the transaction has not be altered in some way – just one character changed would render the mathematics to be incorrect.

Once checked and accepted, the transaction cannot be subsequently repudiated by the sender – no other Private Key could have sent that transaction! You gotta love maths.

BETR assisted the bettor by providing them with a custodial wallet

In the BETR system we understandably wanted to shield our bettors from all this palaver and so we incorporated the signing process in to the BETR application. When a new account was created by a Bettor we create a new Private Key for that account and stored it in our database alongside the other usual account details.

The bettor would be informed only of their Public Key related to their account and so they could then transfer their BETR tokens to that Public Key account and could subsequently place bets.

Crucially, we would fund their account with some ETH to pay for the gas. The bettor could not withdraw (steal) that ETH as they did not ever get access to the Private Key which would be needed for a transfer. This was not so much of an issue at that time as ETH was cheap and it was no skin of our collective noses.

All the bettor then had to do was to select the Event, Bet and Stake and press the Place Bet button. On reception of this demand, the BETR backend would create the Ethereum transaction and sign it using the Bettors Private Key and Bob was your uncle.

What we had created (as we later found out) is termed a custodial wallet – our database held the private keys to which the account holder had no access. With other wallets – such as MetaMask, it works the other way around – only the account owner has access to their Private Key which is termed as a non-custodial wallet.

This approach seemed to solve the problem and made life easier for the bettor. However, experienced blockchain aficionados will immediately see the issue with this idea.

Rising transaction costs were a big problem

As the price of ETH grew, so the cost of placing a bet grew alongside it. And that cost was borne solely by BETR.org. The price of ETH went meteoric. At one point it cost the company around $50 for each bet being placed! Not only that, each bet had to be processed and resulted which cost even more.

Doom and disaster! And so ended BETR.org.

So is there still a future for blockchain betting? You betcha. You’ll be pleased to know that all of these issues (and more) have been solved. So, lets go back to the future of sports betting.

The future of betting!

Finally returning to the actual subject of this article, I am happy to report that the future of sports betting is now clearer to me. And yes, it certainly involves blockchain and a true P2P betting model. This new model is known as Chain.wtf.

However, do strap in, we’re now talking about an exponentially more capable and complex model than that of BETR.org. I’ll do my best to keep it understandable!

Thankfully, with Chain.wtf, we still have entity known as the Bettor who still needs an account and funds. To place a bet a bettor still need to be able to select events, bet types and stake amounts as usual. All good so far.

Chain.wtf being a blockchain solution, the account a bettor needs is a blockchain Public / Private Key and their betting funds are in USDC – a stablecoin where 1 USDC = $1. They need a wallet such as MetaMask to hold their keys and to sign transactions. Nothing particularly new here.

To select events, bet types and to specify their stake, they will need access to a sportsbook frontend website and this also nothing new. However, the bettor will need to ‘log in’ to the website by connecting it to their blockchain wallet as their Public Key will be their account identity.

The future of betting!

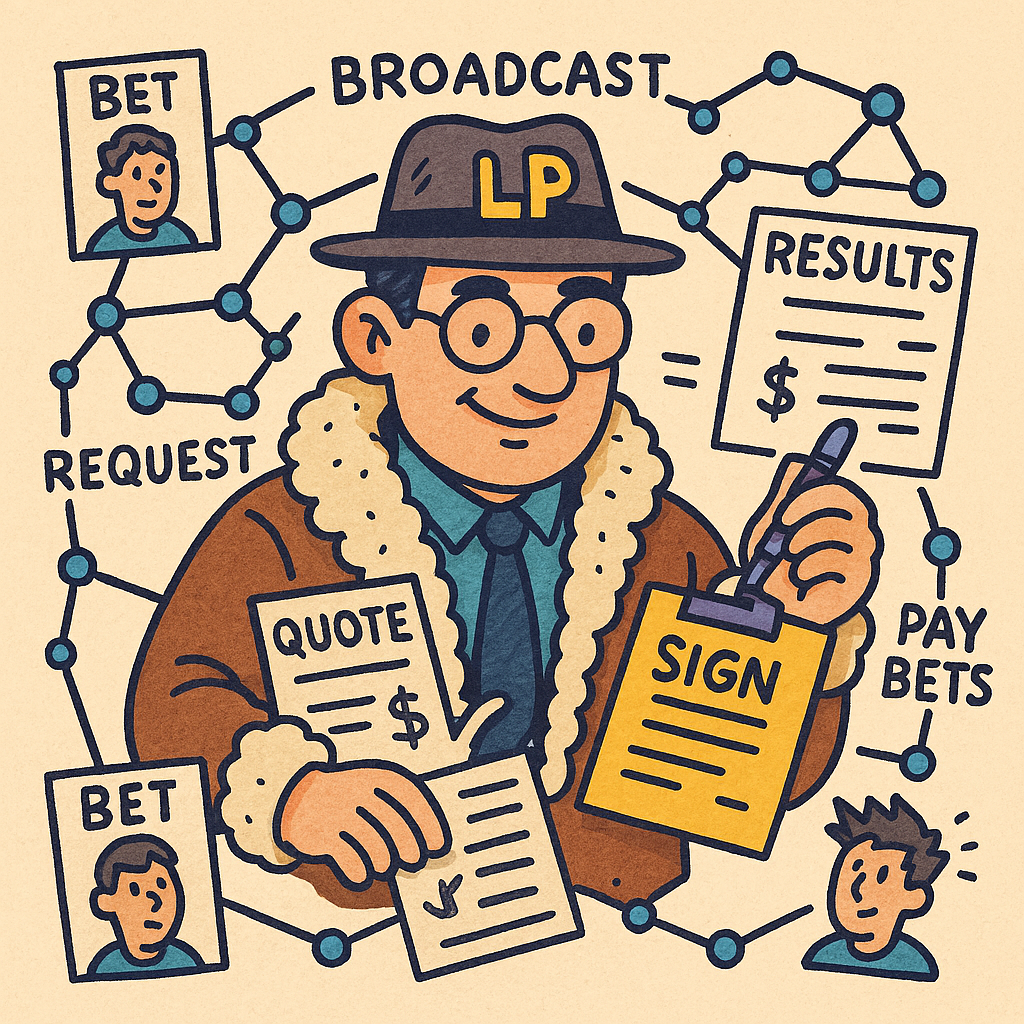

So, who is actually accepting the bets then? Well it’s usually a bookmaker but now we’re going to use the term Liquidity Provider (LP) – an entity who quotes odds, accepts bets and provides the funds to pay the bettor if their bets win.

In the Chain.wtf model, anyone can be a LP and can accept bets. But, how do you as an LP decide whether or not it’s in your interest to actually accept a bet or not? To assist in this decision, the Chain.wtf model introduces an extra step in the betting process – the quotation stage. Let me explain…

There are three factors involved as to whether or not a LP is interested or not in accepting bet. One is the current price, two is their current position and three is do they have enough funds to cover the potential loss.

All of this is automatically managed by the Chain.wtf protocol by the way. And that really means that it is a set of blockchain smart contracts that decides how much to shave odds by in accordance with the LP’s position and decides whether or not to accept the bets.

To elucidate; when a bettor decides to place a bet using the frontend website, the bet data transmitted to the blockchain contains not only the event data, bet type and stake but also contains a figure called the Minimum Acceptable Odds – that is the lowest odds price that the bettor will accept for that bet.

The future of betting!

So, the bet being placed is really only a bet request at this stage, not an actual bet. When it is received by the Chain.wtf protocol, a request is made to a data provider for the current odds which are then adjusted in accordance with each LP’s current position. If the acceptable odds are higher than the minimum odds specified by the bettor, then the bet is confirmed. If not, then the bet is rejected and the stake amount is returned to the bettor.

Interestingly, the Chain.wtf protocol allows for multiple Quote Providers and LPs and will split the bet across LPs if it’s beneficial to do so. This is termed as a blended odds bet. For example, A bet at $100 for 2.5 can be split across one LP for $50 at 2.6 and another for $50 at 2.4. $100 x 2.5 = $250 which is the same as $50 x 2.6 + $50 x 2.4 = $250. The bettor will not see any of this, just that their bet was accepted at 2.5.

So you can see the basic idea. The devils are in the details of course. The first devil is who pays the gas cost? And how can bankruptcy similar to BETR.org be avoided?

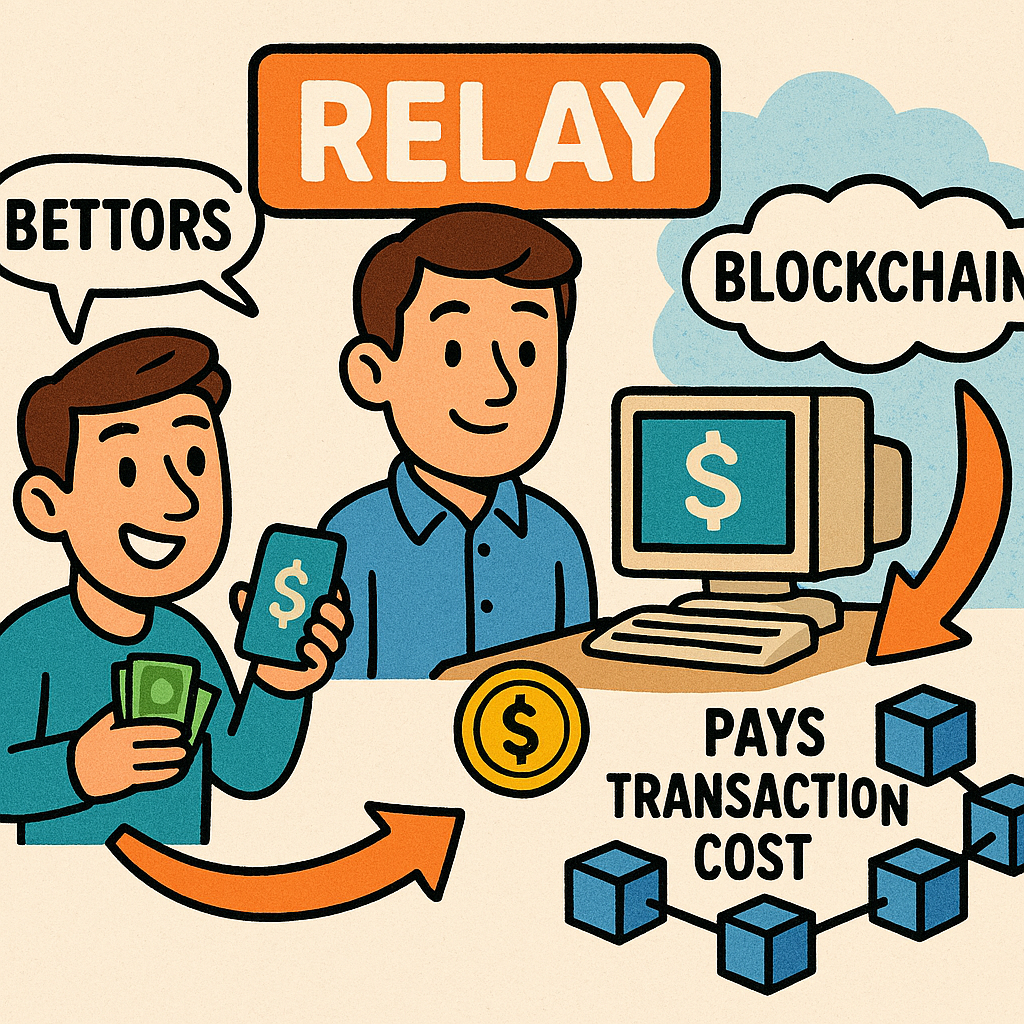

Relays pay for the blockchain transaction cost

To avoid the hassle of the bettor’s wallet needing to hold a blockchain native currency such as ETH to pay the gas fee, the Chain.wtf model employs a service called a Relay. A Relay accepts a signed Place Bet transaction from the bettor and will submit it to the blockchain on the bettors behalf and pays for the gas from it’s own account. The blockchain smart contract will extract the sender’s public key, i.e. the bettor’s account, from the signature rather than from the message sender which would be the Relay.

So even though the Relay pays for execution, the bet still belongs to the bettor because the bettor’s cryptographic signature is what authorises the action. The blockchain contract treats the signature as the source of authority and the relay merely as the messenger that delivered it.

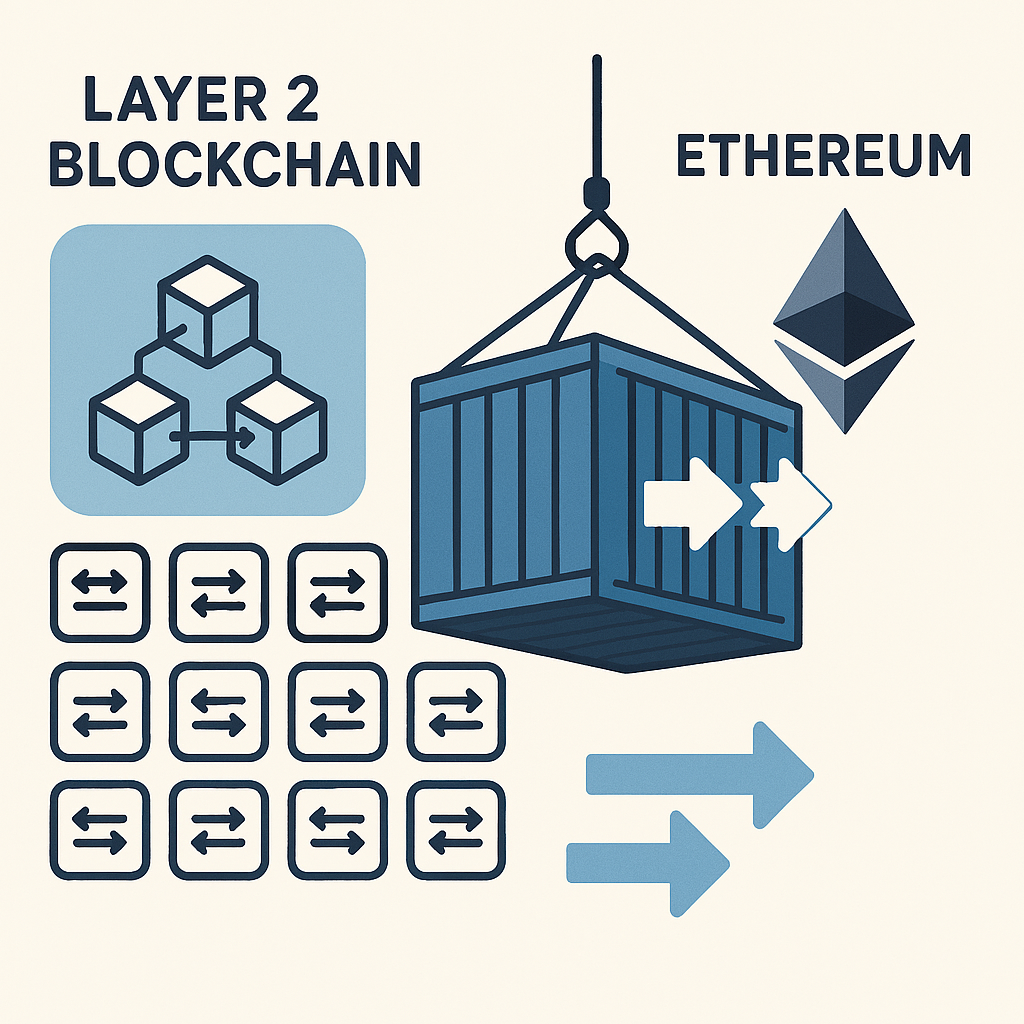

Neat eh? But that doesn’t solve the high cost of ETH does it? Well, because of the high cost of Ethereum transactions, no one in their right mind uses Ethereum blockchain directly anymore. There are these things called Layer 2 (L2) blockchains which are much cheaper and Chain.wtf uses a L2 blockchain called Base.

Layer 2 Blockchains bundle transactions together to reduce the cost

Base is an Ethereum L2 blockchain launched by Coinbase in 2023. It is designed to make Ethereum applications much cheaper and faster while still inheriting Ethereum’s security.

Base does still use ETH for gas as it doesn’t have it’s own native currency. The difference is that the amount of ETH required is dramatically lower than using Ethereum directly. How is this possible? The short answer is that Base processes transactions off the Ethereum main chain and then submits them to Ethereum in batches.

Think of it in terms of shipping containers. With Ethereum a user sends a single package from A to B and pays the full shipping cost. With Base, packages from multiple users are bundled or ‘Rolled Up’ into a container which is then shipped from A to B. The shipping cost is shared amongst all the senders. The container still reaches the same destination, but the cost per package is much lower.

Base transaction fees actually consist of two components, the L2 fee – the cost of processing on Base itself which is usually tiny and the L1 fee – the cost of eventually publishing on Ethereum itself which is often the larger portion of the fee.

In comparison, a bet placed directly on to Ethereum might cost in the region of $20 whereas on Base it costs a fraction of a cent. Base provides the speed and low cost to provide a decent user experience whereas Ethereum provides the security and final settlement. Best of both worlds!

Liquidity Provider

In the blockchain world, transactions are always atomic – that is to say that all parts of the transaction must complete in order for the whole transaction to succeed. For example, A bet placed transaction consists of many smaller transactions that debit the bettors balance, create a bet record, update the odds and so forth.

One part of the place bet process that is unique to blockchain betting is that the potential loss the bet may incur must also be available and locked. This is so that the bet is guaranteed a payout.

So a pool of tokens must be made available to the model to pay potential wins. That is the #1 requirement for a LP – provide liquidity.

And that liquidity needs to be in the form that can be handled by the blockchain, so in crypto tokens. Chain.wtf uses USDC which, being a stablecoin, reduces risk for the holder by always maintaining it’s value, USDC 1 = $1. How it does that is another matter and not one that needs to be addressed in this article – just take my word for it.

As mentioned earlier, the Chain.wtf model also places the responsibility of accepting bets on the LP and when they do so a portion of their pool will be locked to ensure payout in case of a win.

Balancing books is not easy

However, as any good bookmaker knows, the idea is to balance one’s books by attracting bets on all sides of a proposition so that the total stakes will pay the total win with the difference being the bookmakers profit.

To this end, the Chain.wtf model does not just simply lock the potential win for each bet but will take into consideration all of the bets that a LP has accepted on an event and will only lock the maximum liability. This efficient process allows the LP to accept as many bets as possible for both single bets and parlays.

Also, during the quotation process, the LP’s current position is taken into consideration and odds are shaved or increased slightly depending on the desire to attract or discourage betting on an event outcome. This is all handled by the Chaint.wtf smart contracts and happens automatically.

A LP is responsible for a variety of tasks

Remember that we talked about Skype earlier? Skype worked with a bunch of supernodes to handle communications between Skype parties. Each supernode was running a Skype program usually on a PC of some description.

In a similar fashion, the LP needs to run a dedicated application – a node – to handle the various tasks required. The LP can run the hardware infrastructure themselves or can use a managed service for node deployment and maintenance.

Each LP node is responsible for a variety of tasks including:

That’s quite a lot of stuff happening there. And just how is the security handled? Could each node could be manipulated somehow?

Misbehaviour is punished

Well the short answer is of course, yes, there could be an attempt to compromise a node in some way. However, the clever lads have thought of all this and, as with any good decentralized network, there are protocols to prevent this from happening.

Firstly, in order to operate a LP, a bonded stake must be provided. This is basically a deposit that will be confiscated should the LP be up to no good like providing incorrect results or attempting to manipulate the node in anyway.

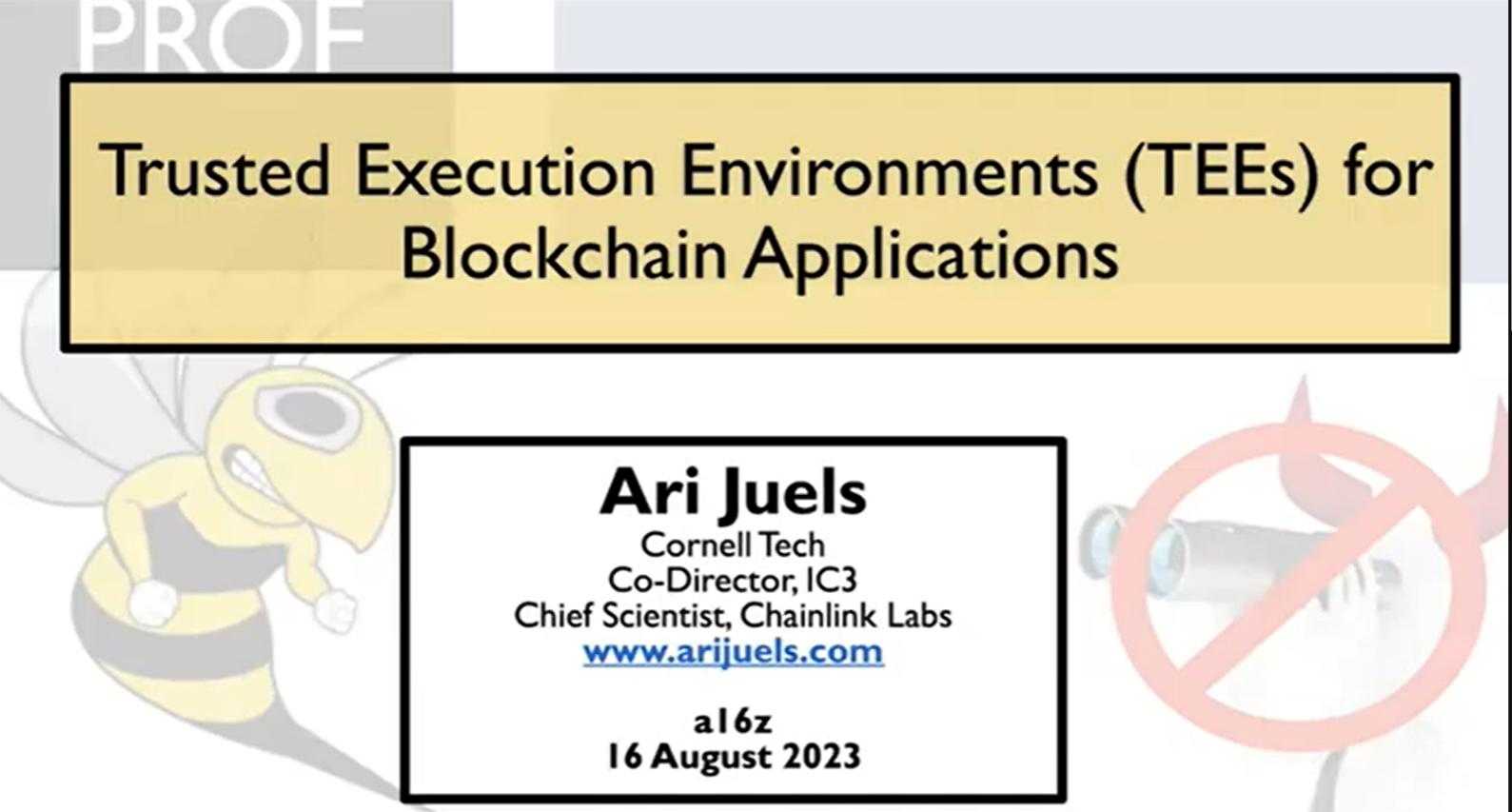

As you may notice from the task list above, the LP’s quote signer service is the heart of the node. And that involves another clever bit of tech called TEE Network.

TEE is cool and explained here at length

The term TEE network usually refers to a blockchain or distributed computing network that uses Trusted Execution Environments (TEEs) as part of its security model.

A TEE is a hardware-protected area inside a CPU where code can run privately and securely, even if the operating system, cloud provider, or server administrator is compromised. TEEs are often called secure enclaves. Code and data inside the enclave cannot normally be viewed or modified by the rest of the machine.

Many modern CPUs provide this feature including Intel SGX, AMD SEV, Intel TDX, ARM TrustZone and AWS Nitro Enclaves.

One of the most important TEE concepts is remote attestation. The enclave can generate a cryptographic proof stating:

I am genuine Intel SGX hardware

I am running this exact code

I have not been modified

External systems can verify this proof before trusting the enclave. This is critical because otherwise users would have no way of knowing whether the node operator changed the software.

The core LP goal is to be a trusted, transparent provider that can sign quotes securely, manage liquidity safely, and survive dispute verification under the protocol’s attestation model. The Chain.wtf LP node relies heavily on the TEE tried and trusted technology to ensure complete security and reliability.

Submit incorrect results and risk a penalty

Ah yes. Importantly, we still have the thorny issue of who decides on which bets to payout and when to do so.

In the old BETR model, the central system would receive event results from a data feed and would process the bets centrally. This was ok if the data feed was 100% correct – which it was not always. When an incorrect result occurred and the bets were incorrectly paid or not paid, this was a huge headache as the transactions on blockchain are undo-able.

In this new truly decentralised Chain.wtf model the same process cannot be employed as there is no central system making decisions and the impact of improperly processed bets should be avoided at all costs.

So, who pays the bettors and when?

The natural proposers for event results are the LPs as they hold the betting exposure. However, it could in theory be anyone, including the bettors themselves.

Of course, the Chain.wtf model cannot trust anyone to do the right thing, so when an Event result is provided it is not taken as gospel until a defined delay (2 hours) has passed. This period of time is called the Dispute Window.

Results can be disputed

During the Dispute Window, the event result as defined by the LP can be challenged by other actors. Should they wish to do so, then the challenge must be accompanied by a verification cost in USDC to deter annoying spam challenges.

If challenged, the Chain.wtf model will dispatch a verification task to a random LP node on the network. The node will then query configured sources and will ultimately return an attested result.

If the result matches the LP result, then the result is confirmed and the smart contract settles the bets.

If the result differs, then the LP that proposed the result is penalised by removing some of their security stake and a bounty is paid to the challenger. The smart contract settles the bets.

If the process fails and automatic verification is unavailable for some reason or another, then the Security Council (see below) may act as a final backstop to finalise the result.

When a bet loses, that is the LP wins, a small protocol fee is put to one side and when all bets for the event have been resulted, the total protocol fees a distributed to the Delegators (see below) based proportionally on shares of bet placement.

Capital Delegators have an easy life

So let’s go back to the components of the Chain.wtf model. We’ve spoken about the bettors and what they need and the Sportsbook Frontends and how they display events and prices. Then we mentioned these new fellows called a Liquidity Provider.

There are many more fellows involved of course. Let’s summarise the situation and introduce some more of these fellows.

So far:

Then then finally there also these roles that are a key part of the Chain.wtf model. The Capital Delegator, The Security Council and Governance.

Let’s take them one-by-one.

A Capital Delegator is a sort of lazy LP. In exchange for providing additional liquidity to a LP, they share in the LP’s profits without having to do any work. However, they must accept a 3 day withdrawal delay to prevent yield sniping attacks around bet settlement.

The Security Council role is there to ensure the correct results are verified.

The role of Governance is to set fees, admit new LPs and set protocol parameters.

You can’t trust anyone…

Sports betting is simple. Someone who wants to place a bet on an event looks for someone that is offering to accept their bet. The person that is offering the bet is traditionally known as the Bookmaker and the person that places the bet is called the Bettor. All good so far.

However, when we consider P2P betting, we’re thinking that each participant has a dual role in that they can both place and accept bets – a P2P participant can be both bookmaker and bettor at the same time.

These two roles are nevertheless distinctly different, not conceptually perhaps but certainly in terms of responsibilities. As with the traditional bookmaker model, each P2P bet is a contractual agreement between two parties. Where P2P betting differs is where trust is placed.

Historically, a bettor will place their complete trust in the bookmaker as they hand over their stake money on the understanding that they will be paid out should they prove to be correct. The trust lies with the bookmaker to pay winning bets. Under this traditional scenario, true P2P betting is never quite attainable as, simply put, in the P2P world, no-one can really trust anyone else.

So, to provide a solution to this new trustless world and for true P2P betting to become possible, there needs to be some form of a sovereign third-party that holds the funds from both sides of the bet while the bet is outstanding.

And this is pretty much how the Chain.wtf betting model works, but instead of employing a third party person, the model employs the blockchain to lock the funds from both sides so guaranteeing the funds to pay a winning bet or a losing stake to the correct party.

While P2P blockchain betting is not exactly a new concept, this latest iteration certainly is. Taking the Skype supernode network model and then adding the missing trust and settlement functions, the Chain.wtf system enables anyone to offer and place bets while at the same time solving the critical blockchain transaction costs issues that plagued BETR.org.

Chain.wtf finally provides the internet with a true P2P betting service and is showing us the way forward.

Will Chain.wtf be successful? I would certainly bet on that! Any takers?